Flood Consultants Network Blog

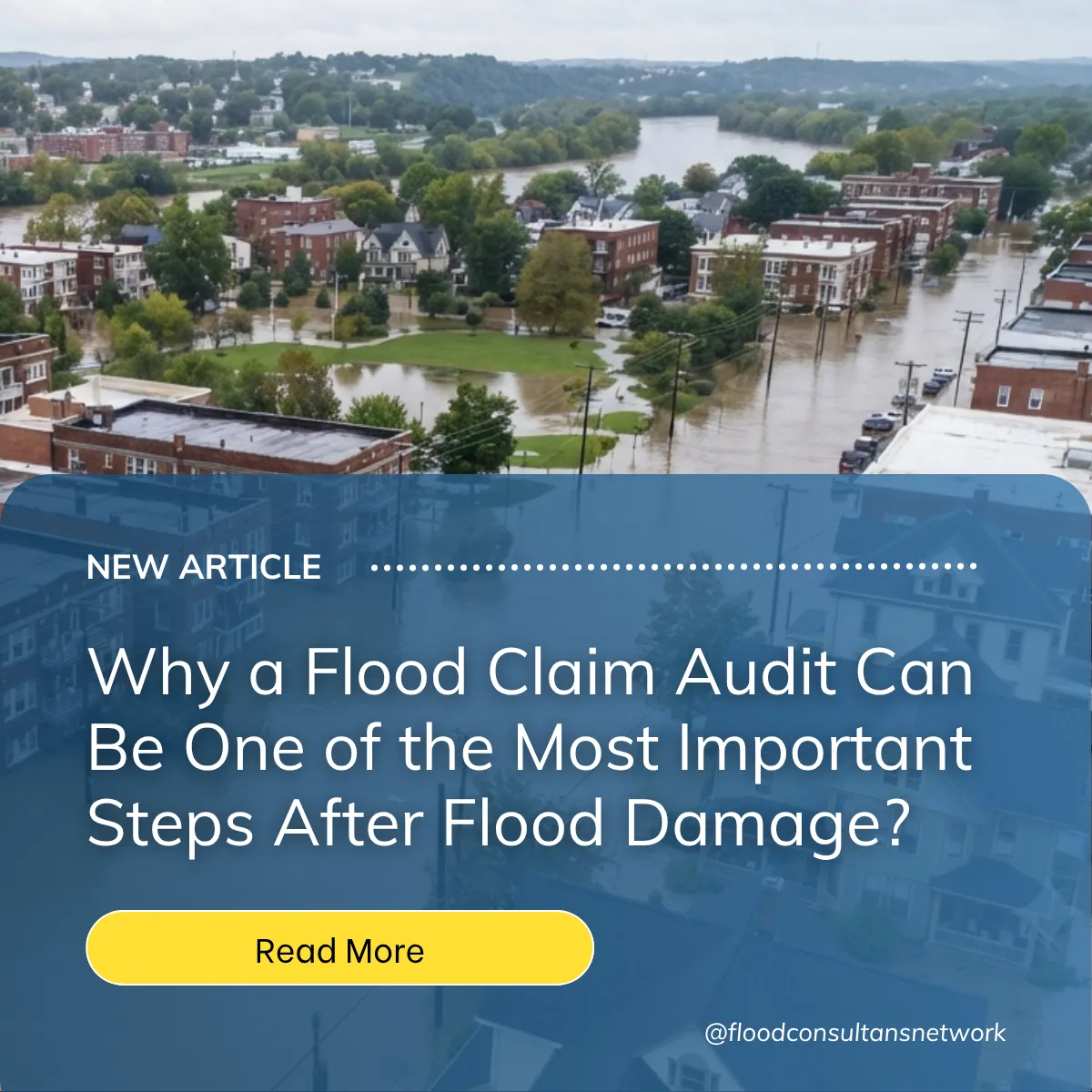

Why a Flood Claim Audit Can Be One of the Most Important Steps After Flood Damage

by: Vance E. Shimley

by: Vance E. ShimleyA flood claim audit helps identify documentation gaps before your claim is truly complete.

Pre-Flood Preparedness

The Most Expensive Assumption Building Owners Make After a Flood

by: Vance E. ShimleyThe biggest flood loss often starts with assuming insurance and contractor costs will match.

Pre-Flood Preparedness

Why Homeowners Still End Up Paying After Their Flood Claim Is Closed

by: Vance E. ShimleyA closed flood claim doesn’t always mean the financial recovery is complete.

Pre-Flood Preparedness

How to Get Flood Adjuster Deployments

by: Vance E. ShimleyFlood deployments go to prepared adjusters, not just certified ones.

Pre-Flood Preparedness

Facebook

Instagram

LinkedIn